- If you are behind in repaying your federal student loans and you collect Social Security benefits, part of your monthly checks could be withheld.

- The reduction is about $2,500 annually on average, a new report from the Center for Retirement Research at Boston College found.

If you are delinquent on federal student loans and collect Social Security benefits, your monthly checks could be reduced.

A pandemic pause has put all garnishments on hold for now.

But when collections are in effect, the reduction in annual Social Security benefits is about $2,500 on average, based on 2019 data, according to new research from the Center for Retirement Research at Boston College.

Get Boston local news, weather forecasts, lifestyle and entertainment stories to your inbox. Sign up for NBC Boston’s newsletters.

That typically amounts to 4% to 6% of household income, a significant amount that could pay off the average person's credit card balance, the research found.

More from Personal Finance:

63% of Americans are living paycheck to paycheck

'Risky behaviors' are causing credit scores to level off

4 tips can help you stay out of debt this holiday season

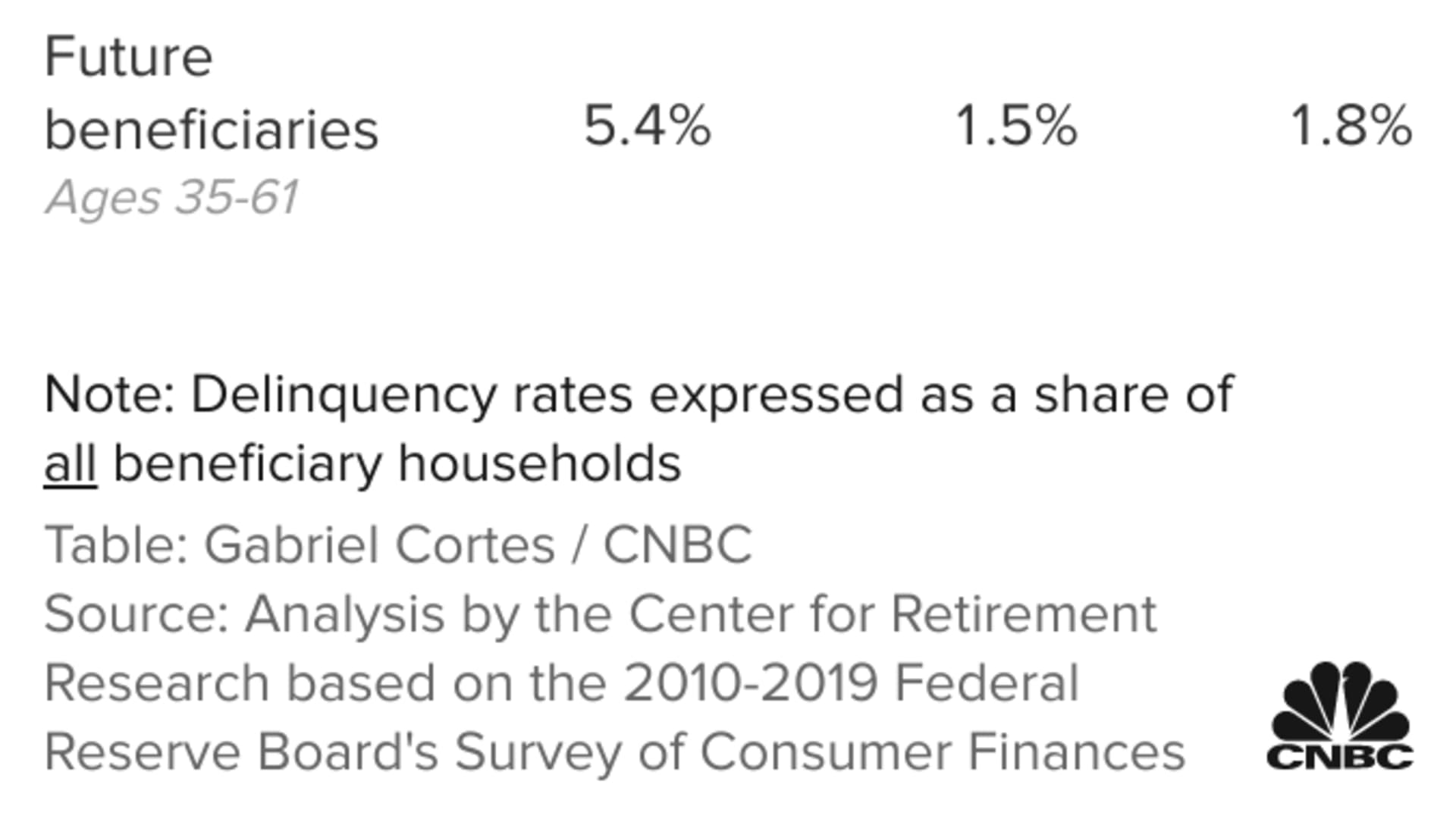

The number of Social Security beneficiaries who find themselves in this situation is small, based on delinquency rates. Less than 5% of beneficiaries currently have student loan debt.

Money Report

But those balances are expected to be "substantially" higher for future beneficiaries, who are also expected to have higher delinquency rates, according to the research.

"Among younger cohorts, the share of people holding student loans are much larger," said Siyan Liu, research economist at the Center for Retirement Research.

"If that continues on into retirement, then a much larger proportion of them, if they have trouble making payments, could be facing benefit upsets," she said.

Social Security benefits are typically subject to partial withholdings after prolonged federal student loan delinquencies.

The Social Security withholding amount for student loan debtors is typically either 15% of the total monthly benefit or the amount by which the benefit exceeds $750 per month — whichever is less.

"It has been a real issue for people who are on a fixed income and have no other support," said Adam Minsky, a Boston-based lawyer specializing in student loan law.

"That 15% really can make the difference between being able to pay for rent or food or medication," Minsky said.

Social Security benefit withholding typically happens after 425 days of delinquency has passed and a loan holder fails to restart repayment.

The money withheld is applied to the federal loan balances.

How much money is at stake

About 2.7 million consumers ages 62 and up owed more than $107.3 billion in federal loans as of September, according to the U.S. Department of Education.

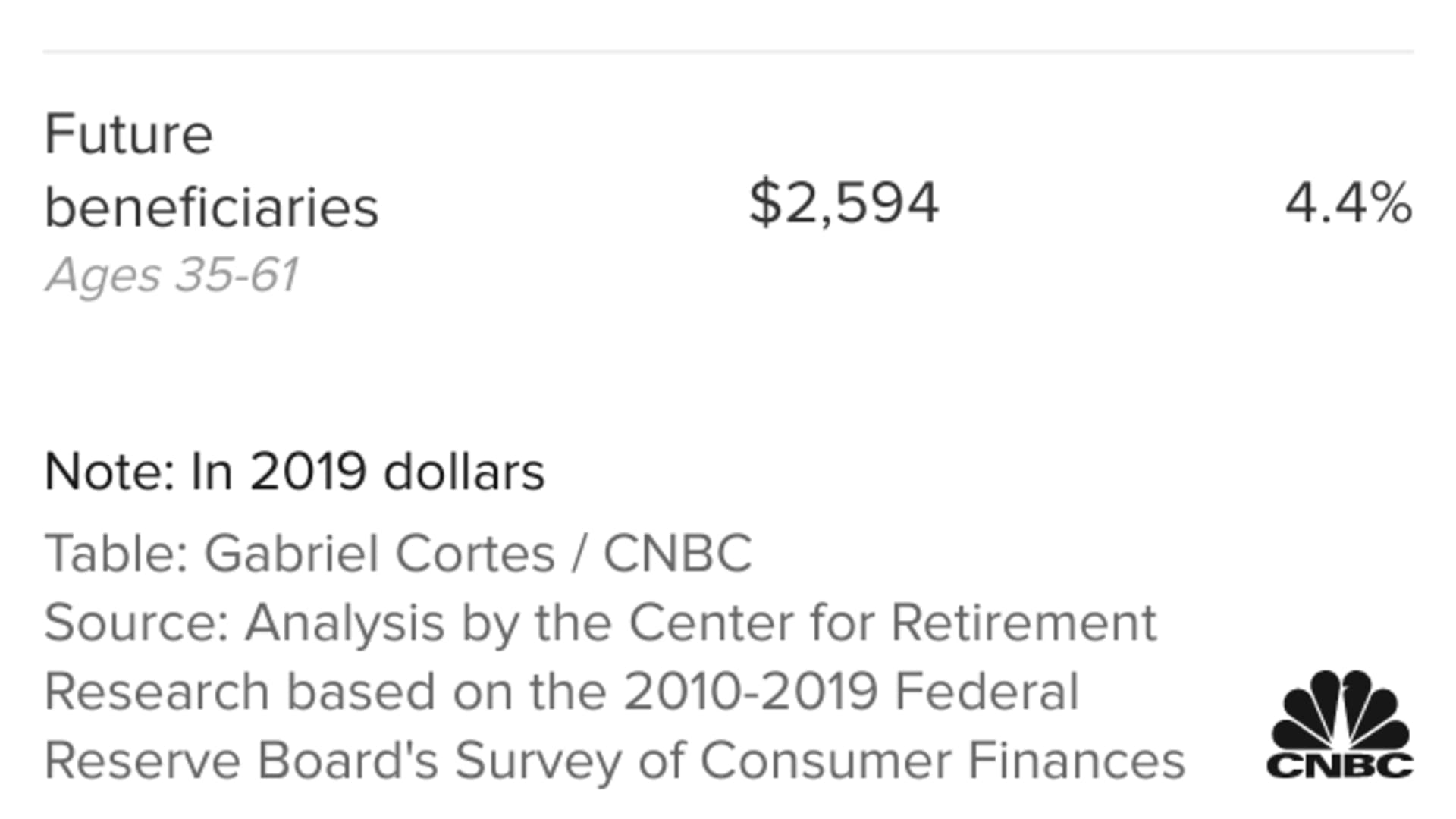

The average annual Social Security benefit at risk due to student loan delinquency is expected to increase to $2,594 for future beneficiaries — those currently ages 35 to 61 — up from $2,299 for current beneficiaries ages 62 and up, based on 2019 data, according to the Center for Retirement Research.

However, the share of household income at risk is expected to decline to 4.4% for future beneficiaries, down from 6.1% for current beneficiaries.

Today's Social Security beneficiaries who are behind on federal student loans are not subject to benefit withholdings, as those collections have been suspended as part of the federal student loan payment pause that has been in effect since March 2020, Minsky noted.

"No one is having their Social Security checks garnished right now," Minsky said.

President Joe Biden's Fresh Start initiative is slated to give borrowers a full year after the payment pause ends to try to get out of default before collections on benefits resume, he noted.

How policy may influence debts

Biden has proposed broad student loan forgiveness of up to $10,000 for federal student loans, or up to $20,000 for Pell grant recipients.

The fate of the plan is now in the hands of the U.S. Supreme Court, which is scheduled to consider it in February.

If the plan goes through, it would result in an average forgiveness of $12,000 per borrower, according to the Center for Retirement Research.

Both Black and Hispanic households, who are more likely to have Pell grants, would have their share of debt holders cut in half, the research found. The share of Black borrowers with debt would be reduced to 12% from 22%.

Yet future beneficiaries in those groups are currently expected to see their delinquency rates rise, according to the Center for Retirement Research.

The plan would also have a dramatic impact on delinquency rates, as delinquent borrowers could have their entire balances forgiven.

While Black borrowers stand to see the largest decrease in delinquency rates, Hispanic borrowers would see the largest relative decrease, the research found.

Because Biden's plan would reduce both debt and delinquency for future retirees, it would also shrink racial inequality, the Center for Retirement Research said.

Some Democratic lawmakers are also eyeing another way of providing relief.

In December, four House Democrats introduced a bill, the Student Loan Relief for Medicare and Social Security Recipients Act, that would eliminate student loan debt balances held for more than 20 years by Medicare and Social Security disability insurance beneficiaries.

It remains to be seen whether the proposal may gain traction on Capitol Hill.

"We should eliminate as much student debt as we can for everyone, but especially for those who have spent decades of their lives working to pay it off," Rep. Adam Schiff, D-Calif., said in a statement. "This bill would ensure that instead of triaging their benefits, seniors and disabled individuals can focus more on their health, their families, and thriving in their best years."