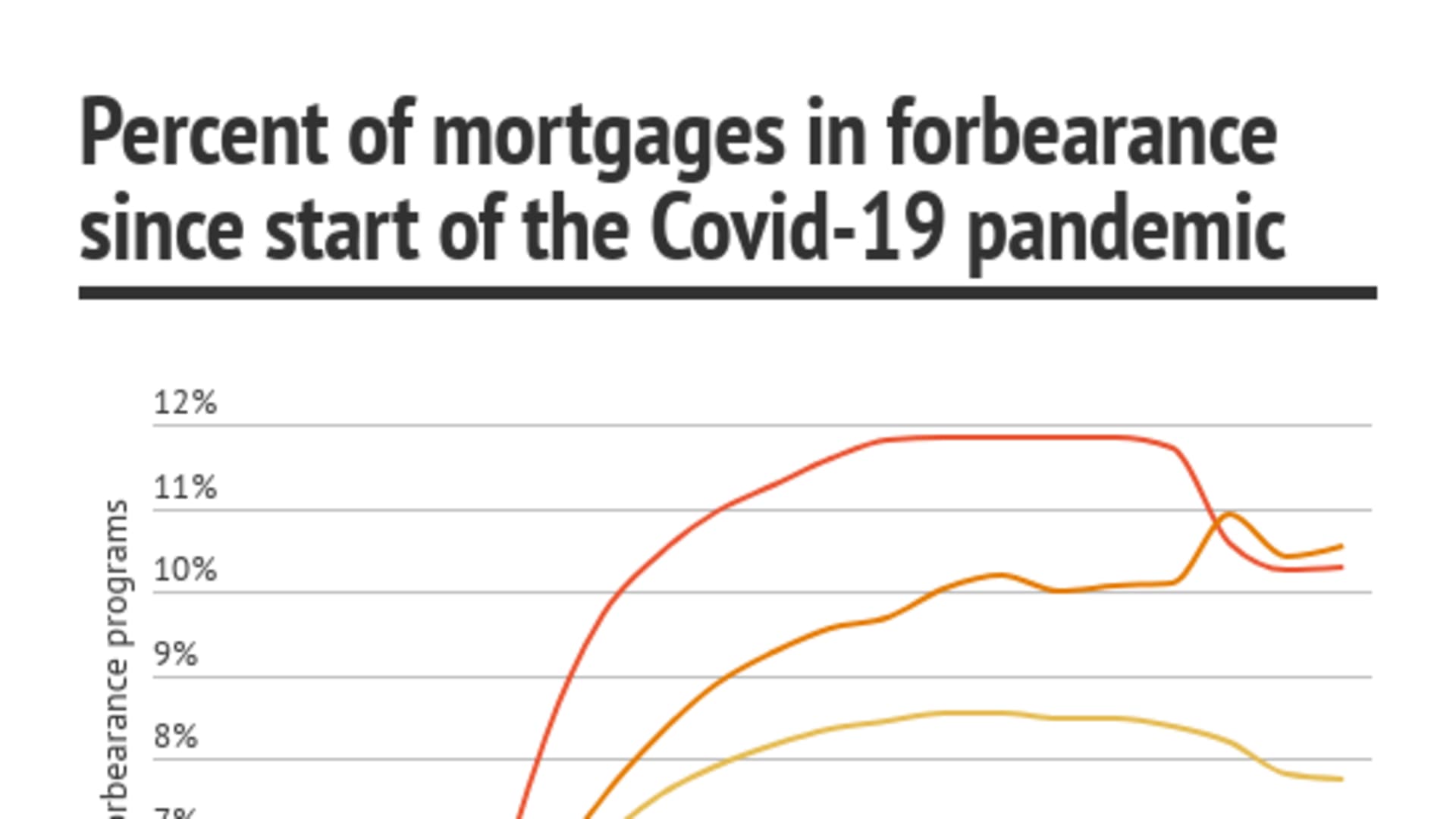

Nearly four months after banks and federal agencies started offering a number of assistance programs aimed at giving Americans a break on their mortgages, about 4.1 million homeowners remain in forbearance plans.

But that number is starting to shrink as more workers are called back to work, says Mike Fratantoni, chief economist for the Mortgage Bankers Association, which produces the Forbearance and Call Volume Survey each week. As of July 5, 8.18% of all active mortgages are in some type of government or private-sector forbearance program. That's down slightly from the high in early June of 8.55% of mortgages in forbearance.

Congress enacted the CARES Act in March that, along with federal guidelines, gave homeowners with federally backed loans two major forms of relief. First, lenders are barred from starting foreclosure proceedings on federally backed loans until at least August 31, 2020.

Second, it gave homeowners with government-backed loans who are experiencing financial hardships because of Covid-19 the option to request up to 180 days of forbearance on their mortgage. That forbearance allows you to pause or reduce your mortgage payments, but it's not loan forgiveness. If, after six months, you're still experiencing financial difficulties, you can request up to another 180 days.

Yet those with mortgages owned by private lenders, such as banks, are not included in this relief. About 30%, or roughly 14.5 million U.S. mortgages, are privately owned and not backed by any federal agency, according to the National Housing Law Project. Just under 11% of these privately-held mortgages remain in some type of forbearance or deferment program, a higher level than that of Americans with government-backed loans.

"It doesn't mean that the consumers are not getting the help. It just means there is no standard here because different banks may do things differently," says Karan Kaul, a research associate in the Housing Finance Policy Center at the Urban Institute.

Money Report

Fannie Mae and Freddie Mac offer loan lookup tools that can help you quickly determine if either of these major lenders owns your loan, but you can also always ask your servicer or look at your loan documents.

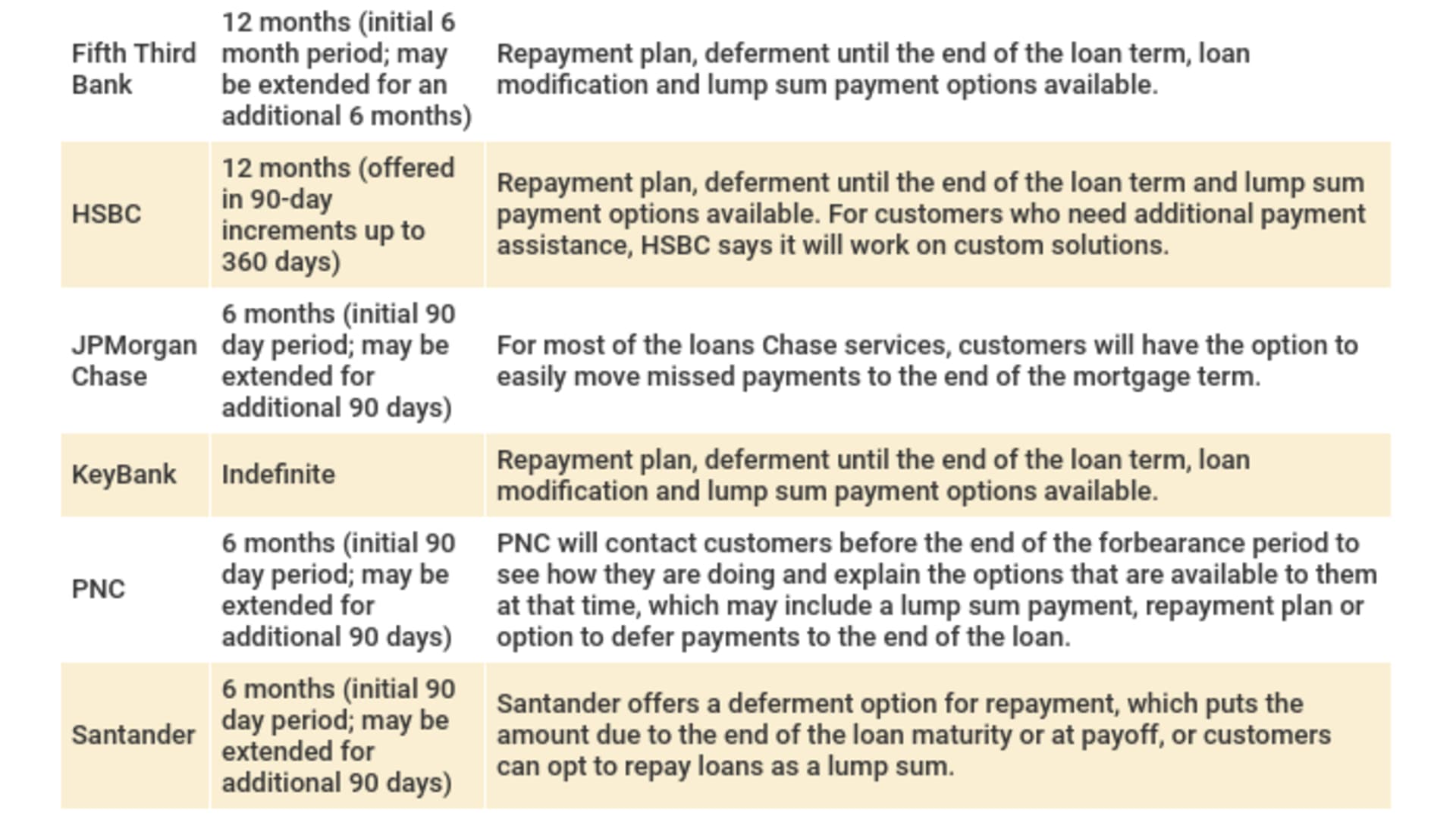

CNBC Make It reached out to 16 major banks that had previously announced Covid-19 mortgage assistance programs in March and a dozen banks responded that they are still offering these relief measures and detailed what was available. While banks have set up programs that basically follow the federal guidelines, CNBC Make It found the forbearance periods, terms and repayment options did vary from bank to bank.

Many of the banks initially offered 90-day forbearance periods, but all have now extended those programs to last at least six months. And while homeowners were concerned at first that they would have to repay their missed mortgage payments as a lump sum, most banks now offer several additional options:

- A repayment plan allows homeowners to pay an extra amount along with their regular mortgage payment to repay the skipped payments in forbearance.

- A deferment plan allows homeowners to push the amount due to the end of the loan term. Depending on the program, this amount may be due as lump sum payable upon maturity, payoff or finance of the mortgage.

- A loan modification allows homeowners to apply to have their loan interest rate reduced, extend the term of the loan and/or reduce their monthly payments.

Not every bank is offering these programs and not every mortgage is eligible for all of the repayment options, says Lisa Sitkin, senior staff attorney with NHLP. "There's a lot of uncertainty," she says.

That's because many times, banks act as a homeowner's loan servicer, but a private lender or investor may actually own the mortgage. They simply use the bank to service the loan by collecting payments and making sure the tax authorities, homeowners' insurance and loan repayments are taken care of.

And often those investors have agreements in place with the bank that puts restrictions on how much flexibility the loan servicer can provide when it comes to the loan payments and mortgage terms.

"Unlike with the federally backed [mortgages] where there's publicly available guidance about what the servicers are supposed to do, in the private sphere we don't have direct access, or easy access, to these agreements that the servicers rely on," Sitkin says.

A payment deferral, for example, can be handled a couple of different ways. Most people, when they hear about deferring the payment to the end of the loan think that if you were on forbearance for six months, the mortgage will just be extended for six months, and the borrowers will just make those payments then.

But Sitkin says that for a lot of these deferment programs, both federal or private, the loan servicer is going to take those missed payments, put them in a separate pot where no interest is added and then that amount becomes due as a lump sum when your loan matures.

"For some people, that's still going to be hard to pay, especially if you were much farther along than your loan," Sitkin says.

Some homeowners may find themselves in the position of applying for a loan modification to reduce their monthly payments or change the terms of the mortgage, including the length. But you're not guaranteed to get a loan modification. If somebody's household income is severely diminished and needs to reduce their monthly payment, for example, they may get the answer from the bank: 'We can't make it work,' Sitkin says.

At the end of the day, experts say getting in and out of forbearance will be a challenge for homeowners. "It is going to be difficult for folks to navigate. They will almost always be better off if they are working with a housing counselor or some other type of advocate, but the reality is we don't have those resources for everybody," Sitkin says. The CFPB offers a Find a Counselor tool, which provides a list of counseling agencies that can help advise on loan terms, credit issues and foreclosure.

When it comes to working through this process, Sitkin says it's a fine line between being an advocate for yourself and accepting what you can't change. Once you've agreed to a relief program, ask your loan servicer to provide written documentation that confirms the details of your agreement. And if you have questions about your ongoing forbearance, you do have the right to send in what's called a request for information and the loan servicer is required to respond within 30 days.

"You can push back, and you should ask for more information," Sitkin says. "I don't like to tell anyone to take at face value what the servicer is telling you. On the other hand, there is enormous discretion, whether we like it or not, in the private market about how these things are going to be handled," she says, adding that she doesn't want people to be under the impression that they have certain rights or are entitled to certain things.

"I've just seen many too many people spend enormous amounts of time and energy and get themselves into a worse position," Sitkin says.

But just because it may be challenging or potentially uncomfortable, doesn't mean homeowners shouldn't attempt to get the assistance they need, Kaul says. "There's absolutely nothing to be embarrassed about — if you're impacted by Covid, it's not your fault. This is something that will help you preserve your liquidity."

Check out: The best credit cards of 2021 could earn you over $1,000 in 5 years

Don't miss: 17.6 million unemployed Americans probably won't return to their pre-pandemic jobs