- The Covid relief bill is up in the air as lawmakers battle over raising stimulus payments to $2,000. The measure also includes incentives for donating cash to charity.

- Joint filers who don’t itemize deductions on their tax returns may be able to take an above-the-line deduction for up to $600 in cash contributions to charity starting in 2021. That’s up from $300.

- Taxpayers who itemize deductions on their tax returns can make a cash donation to charity and deduct up to 100% of their adjusted gross income in 2020. Lawmakers want to extend this to 2021.

Giving to charity is about to pay off a little more — that is, if the latest Covid relief bill becomes law.

The $908 billion pandemic relief bill features $600 stimulus checks, $300 unemployment supplement payments and a second round of forgivable loans for small businesses.

It also sets a host of changes to the tax code, including an extension of incentives to encourage taxpayers to donate to worthy causes.

Don't overhaul your tax plans just yet. President Donald Trump hasn't signed off on the legislation. In fact, he ordered lawmakers to revise the bill and include $2,000 stimulus payments to households.

In the meantime, here's what you should know about the charitable giving provisions in the measure — should it become law.

$600 above-the-line break for married couples in 2021

Money Report

The CARES Act, which was passed in the spring, established an above-the-line deduction, allowing a write-off of up to $300 in cash donations to charity this year.

You can also qualify for the break if you make a donation with your credit card or you write a check to the charity.

It's available to filers who take the 2020 standard deduction of $12,400 for singles or $24,800 for married couples.

In the new proposal, lawmakers call for increasing the write-off to $600 for joint filers starting next year. It will still be $300 for single taxpayers.

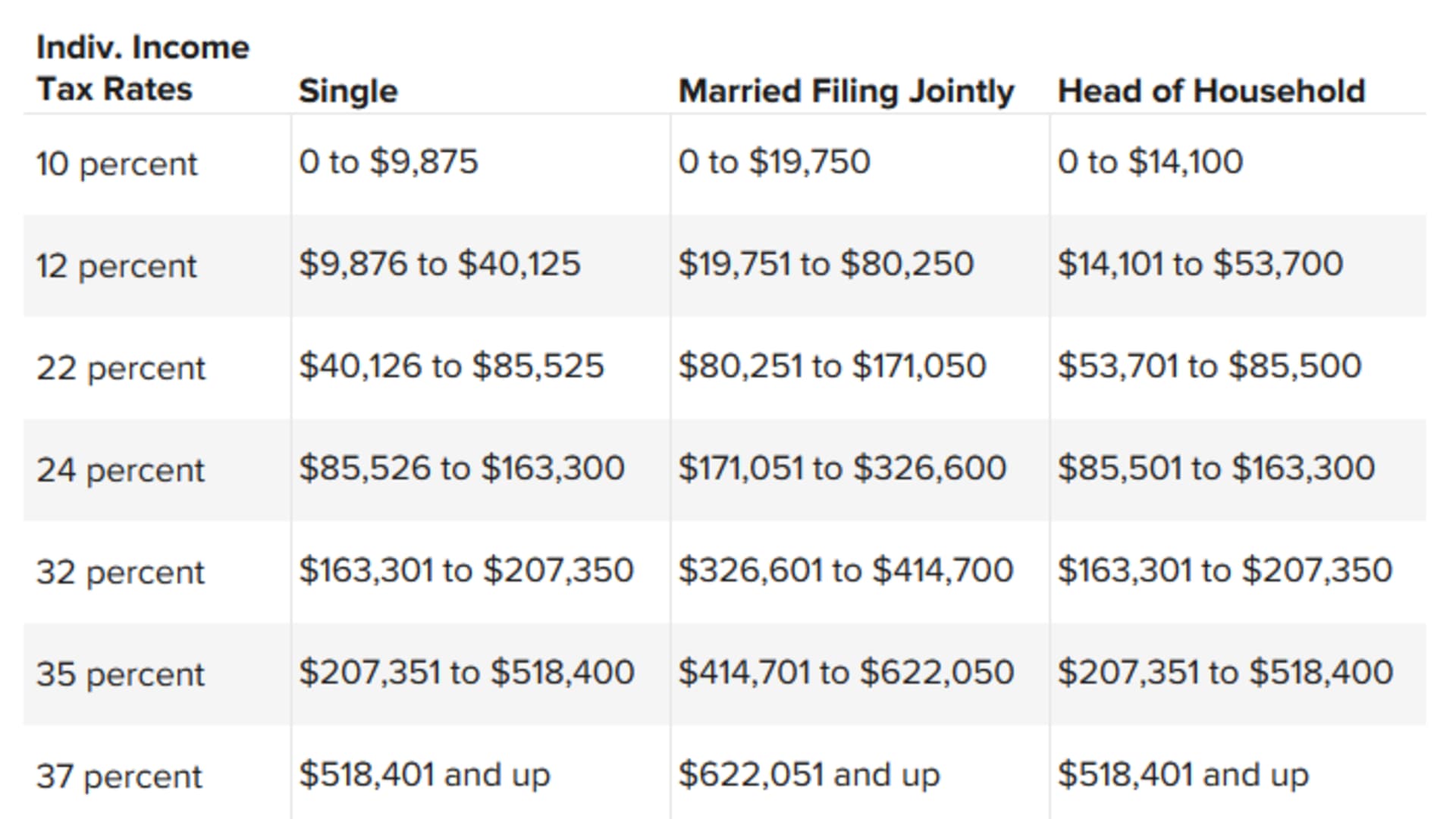

Remember that deductions lower your taxable income based on your income tax bracket. That means the higher your bracket, the greater your tax savings.

Essentially, a $300 deduction is worth $30 to a taxpayer in the 10% tax bracket, but it's worth $111 to someone who's in the 37% tax bracket.

"If you're in the 12% or 22% bracket, what's the benefit?" said Brad Sprong, national tax leader for KPMG Private Enterprise. "The optics are powerful versus the dollar amount."

Even with the low threshold, taxpayers should remember to retain any receipts or acknowledgement substantiating the contribution.

Donors must hold onto this documentation for any donation of more than $250.

Legislators also called for cracking down on taxpayers who fudge the amount they give to charity.

Filers who inflate the deduction and wind up short on their taxes would be on the hook for a penalty of 50% of the underpaid tax, according to the bill. That's up from a 20% penalty.

Itemizers: Larger deductions for cash donations in 2020, 2021

For 2020, the CARES Act also allowed a more generous write-off for donors who itemize deductions on their tax returns.

This year, those households can deduct up to 100% of their adjusted gross income on cash donations made to qualifying charities. Private foundations and donor advised funds are excluded.

Normally, you can write off up to 60% of your AGI for cash donations.

Lawmakers want to extend the heftier deduction for cash into 2021, according to the relief bill text.

The target audience for big cash donations here might be retirees with sizeable assets, rather than people who are still working and saving for retirement.

"It would clearly be someone with a lot of wealth but not much income," said Sprong of KPMG. "They might have municipal bonds and Social Security that's subject to little tax."

As attractive as the larger deduction may seem, cash is probably the least tax-efficient way to donate.

A smarter tax-planning play would be to donate appreciated assets, including stocks or mutual funds, directly to a charitable organization.

By doing so, you avoid the tax hit you'd otherwise face for liquidating them and you nab a write-off for the fair market value of the investment.

"Donating stock is always a really great tip because you don't have to realize those huge gains," said Lisa Greene-Lewis, CPA and TurboTax expert. "People did see some big gains this year."

Be sure you've held the asset for at least a year in order to deduct the fair market value. Otherwise, you can only deduct your cost basis — or your original investment in the asset.

"That's a surprise sometimes," said John Voltaggio, senior vice president, wealth management at Northern Trust. "You can donate the stock to charity, but you need to have it for at least 12 months to get that favorable treatment."