Where you live can drastically affect the long-term value of your home, according to a recent SmartAsset study.

SmartAsset examined home prices dating back to 1997 across 400 metropolitan areas in the U.S. and ranked each based on home value growth and price stability, which is the probability that a home will experience a price decline of 5% or more at any point in the 10 years after it is purchased.

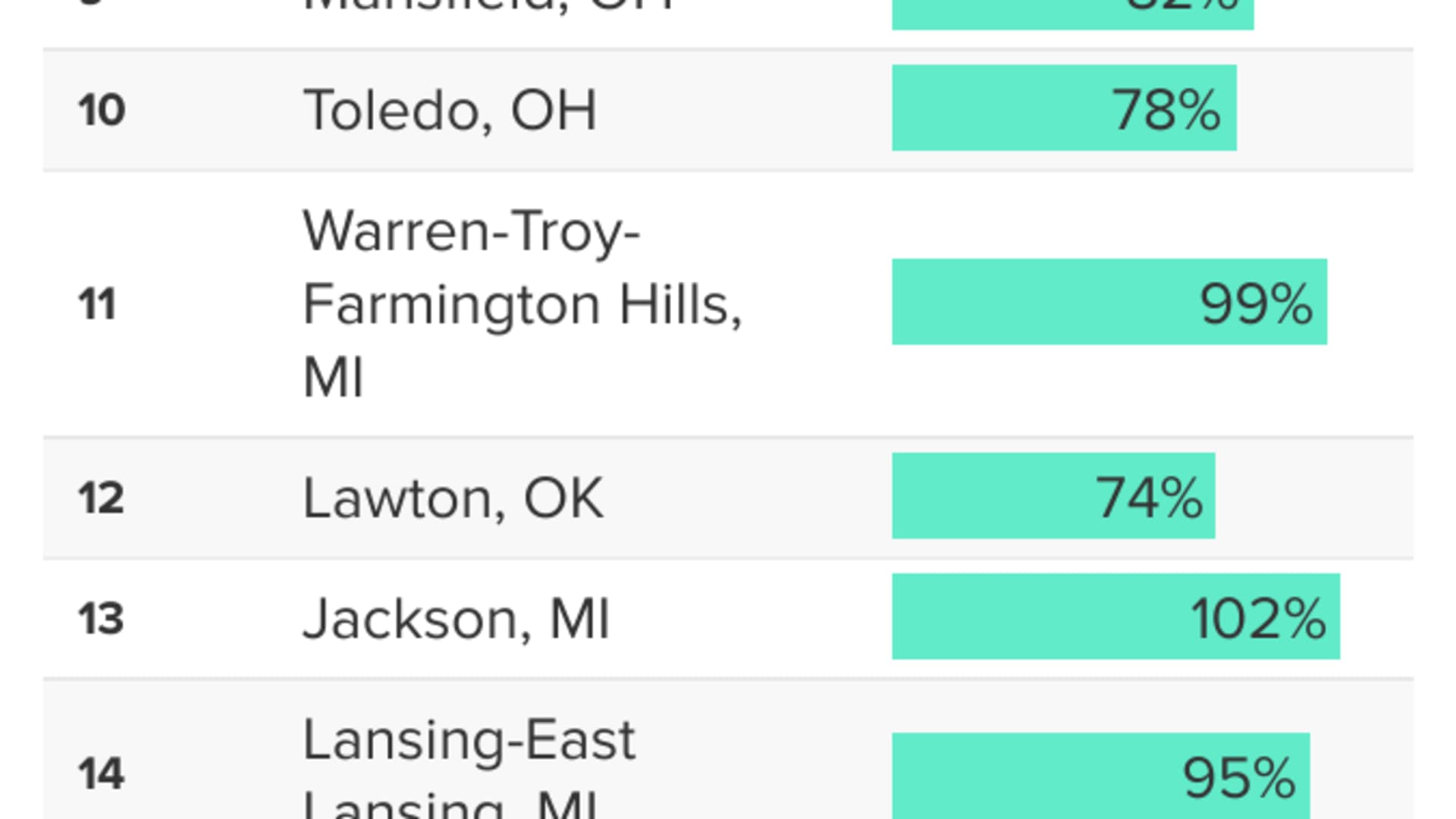

While top markets like Austin, Texas, have seen home price growth of 384% since 1997, homes in the 15 bottom-ranked markets have only increased in value by an average of 84% in that time.

The lower-ranked markets tend to be in so-called rust belt states: former manufacturing hubs that have experienced long-term industrial declines. These include Ohio, Pennsylvania, West Virginia, Wisconsin and Michigan.

Get Boston local news, weather forecasts, lifestyle and entertainment stories to your inbox. Sign up for NBC Boston’s newsletters.

While past performance does not guarantee future results, the study provides some insight into a given market's desirability over time.

Homes offer utility, not just value

Money Report

As an investment, the annual return on home prices varies widely depending on the local market. And generally speaking, the stock market offers better long-term returns and more liquidity.

However, homes aren't just financial assets. They offer utility as places that you can live in for decades.

Owning a property provides some cost certainty to your budget as well, as monthly mortgage payments tend to be predictable and stable over time. This is especially important for people on fixed incomes, like retirees, or people who aren't able to work.

Plus, with home ownership, thousands of dollars that would have otherwise been spent on rent payments goes toward an asset that you will ultimately own and can sell later. And since interest on your mortgage is tax deductible, your annual taxable income can potentially be reduced by thousands of dollars.

Additionally, with a sizable down payment, home ownership can lower your monthly costs compared to renting, making it easier to budget for other expenses.

Sign up now: Get smarter about your money and career with our weekly newsletter

Don't miss: Why a 26-year-old with $350,000 in student loans won't use a credit card