- If you’re trying to max out the yearly purchase limit for Series I bonds, you can buy an extra $5,000 paper I bonds with your tax refund.

- While I bonds are currently paying 6.89% annual interest through April, the rate may decline in May as inflation eases, making alternatives more attractive.

If you're trying to max out the yearly purchase limit for Series I bonds, your tax refund offers an opportunity to buy even more.

However, you should consider your goals and weigh alternatives first, experts say.

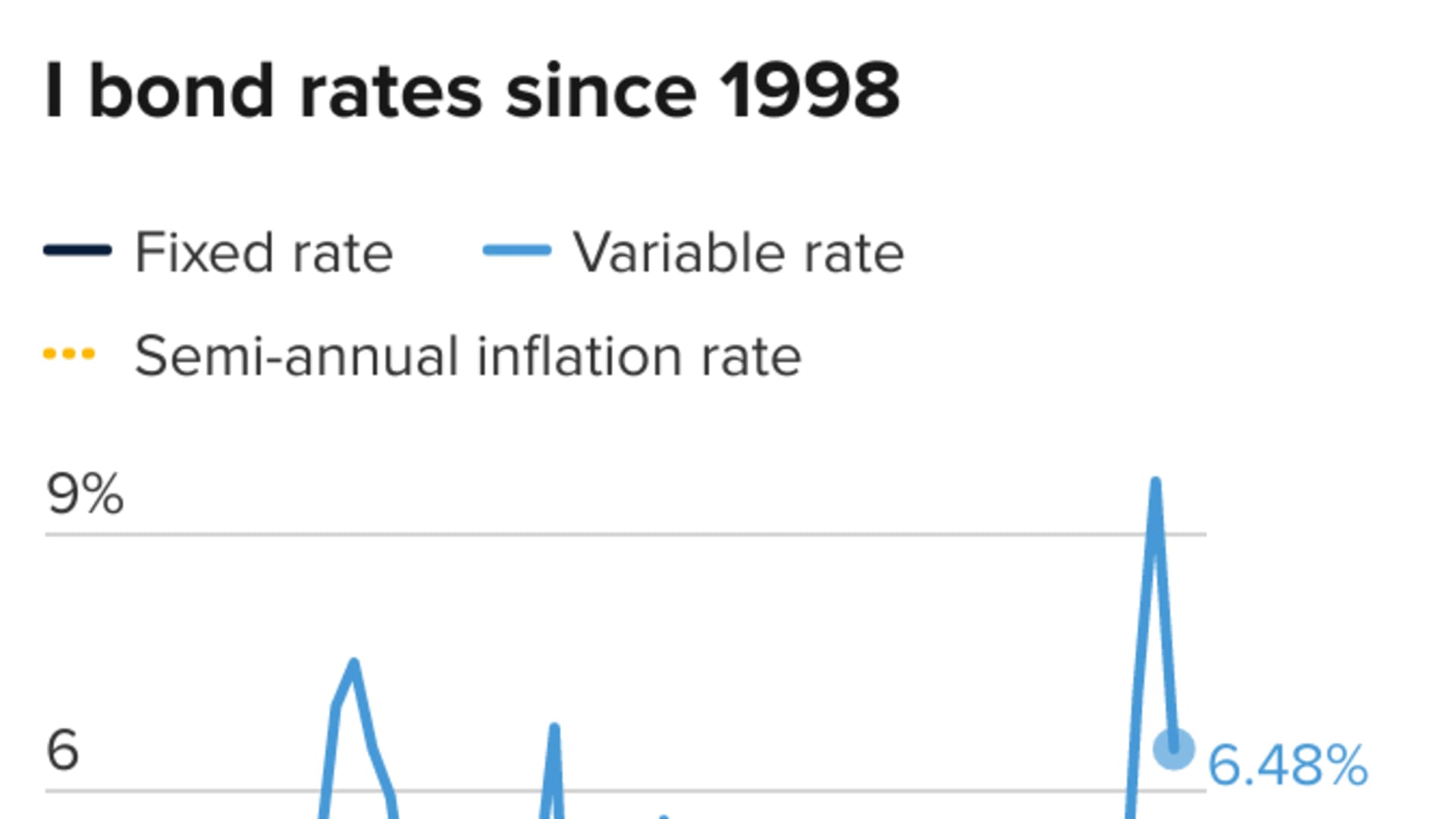

An inflation-protected and nearly risk-free investment, I bonds are currently paying 6.89% annual interest on new purchases made through April 2023, the third-highest rate since they were introduced in 1998.

Get Boston local news, weather forecasts, lifestyle and entertainment stories to your inbox. Sign up for NBC Boston’s newsletters.

While the annual purchase limit is generally $10,000 per person for electronic I bonds, you can buy another $5,000 in paper I bonds with your tax refund.

Buying paper I bonds with your tax refund may make sense if you're eager to purchase as much as possible, said Ken Tumin, senior industry analyst at LendingTree and founder of DepositAccounts.com, a website that tracks I bonds, among other assets.

There are two parts to I bond interest: a fixed rate, which may change every six months for new purchases but stays the same after the bonds are bought, and a variable rate, which changes every six months based on inflation. TreasuryDirect announces new rates every May and November.

But with inflation falling, Tumin said, I bond investors "might be a little bit disappointed in May," noting the combined rate may drop below the past three updates — 6.89% in November, 9.62% in May and 7.12% in November 2021.

Money Report

Treasuries, high-yield savings are smart alternatives

As the Federal Reserve continues to raise the target federal funds rate, other assets have become more attractive, experts say.

"No one should buy I bonds with their tax refund" unless the purchase is part of a long-term strategy to lock in the current 0.4% fixed rate above inflation, said Jeremy Keil, a certified financial planner with Keil Financial Partners in Milwaukee.

For shorter-term goals, Keil points to assets such as Treasurys, high-yield savings accounts or certificates of deposit, with rates that have crept up over the past year.

"Right now it's really easy to get over 4% from an online savings account," said Tumin, noting that rates are the "highest in more than a decade."

He said shorter-term CDs are paying higher rates than longer-term CDs because many institutions are expecting the Fed to start cutting rates in a year or so.

Downsides of paper I bonds

Keil said it's also important to consider the downsides of purchasing paper I bonds tied to your tax return.

"You don't have much control over the timing of the paper I bonds purchase, so don't expect to get the current 6.89% rate unless you file your return well before the deadline," he said.

What's more, paper I bonds must be converted to electronic form before redemption. "It's a long process," he said. "It's not liquid at all."