Amid Inflation, More Middle-Class Americans Struggle to Make Ends Meet

- Many people still identify with being in the middle class, although that doesn’t mean what it used to.

- Inflation is largely to blame.

As inflation spiked, Americans in the middle class were particularly hard hit.

For them, prices increased faster than their income, according to a September report by the Congressional Budget Office. Households in the lowest and highest income groups saw their income grow faster than prices over the same time period, the report found.

Get Boston local news, weather forecasts, lifestyle and entertainment stories to your inbox. Sign up for NBC Boston’s newsletters.

Even though middle-class wage growth is high by historical standards, it isn’t keeping up with the increased cost of living, which in December was up 6.5% from the prior year — making it harder to live the same lifestyle previous middle-class generations did.

More from Personal Finance:

4 key money moves in an uncertain economy

Here's the best way to pay down high-interest debt

63% of Americans are living paycheck to paycheck

Nearly three-quarters, or 72%, of middle-income families say their earnings are falling behind the cost of living, up from 68% a year ago, according to a separate report by Primerica based on a survey of households with incomes between $30,000 and $100,000. A similar share, 74%, said they are unable to save for their future, up from 66% a year ago.

Money Report

The middle class is shrinking

Economists' definitions of middle class vary. The Pew Research Center defines middle class as those earning between two-thirds and twice the median American household income, which was $70,784 in 2021, according to Census Bureau data. That means American households earning as little as $47,189 and up to $141,568 are technically included, although the median income is roughly $90,000.

As is often cited, the share of adults who live in middle-class households is shrinking. Now, 50% of the population falls in this group as of 2021, down from 61% 50 years earlier, according to Pew.

Their share of the country’s wealth is also getting smaller, while the top 1% continue to amass more and more, several other studies show.

'It is only going to get worse'

Financial well-being is deteriorating overall, according to a recent "Making Ends Meet" report by the Consumer Financial Protection Bureau.

Across the board, households have been slow to adjust their spending habits. Even as prices rise significantly, consumer spending hasn’t changed that much.

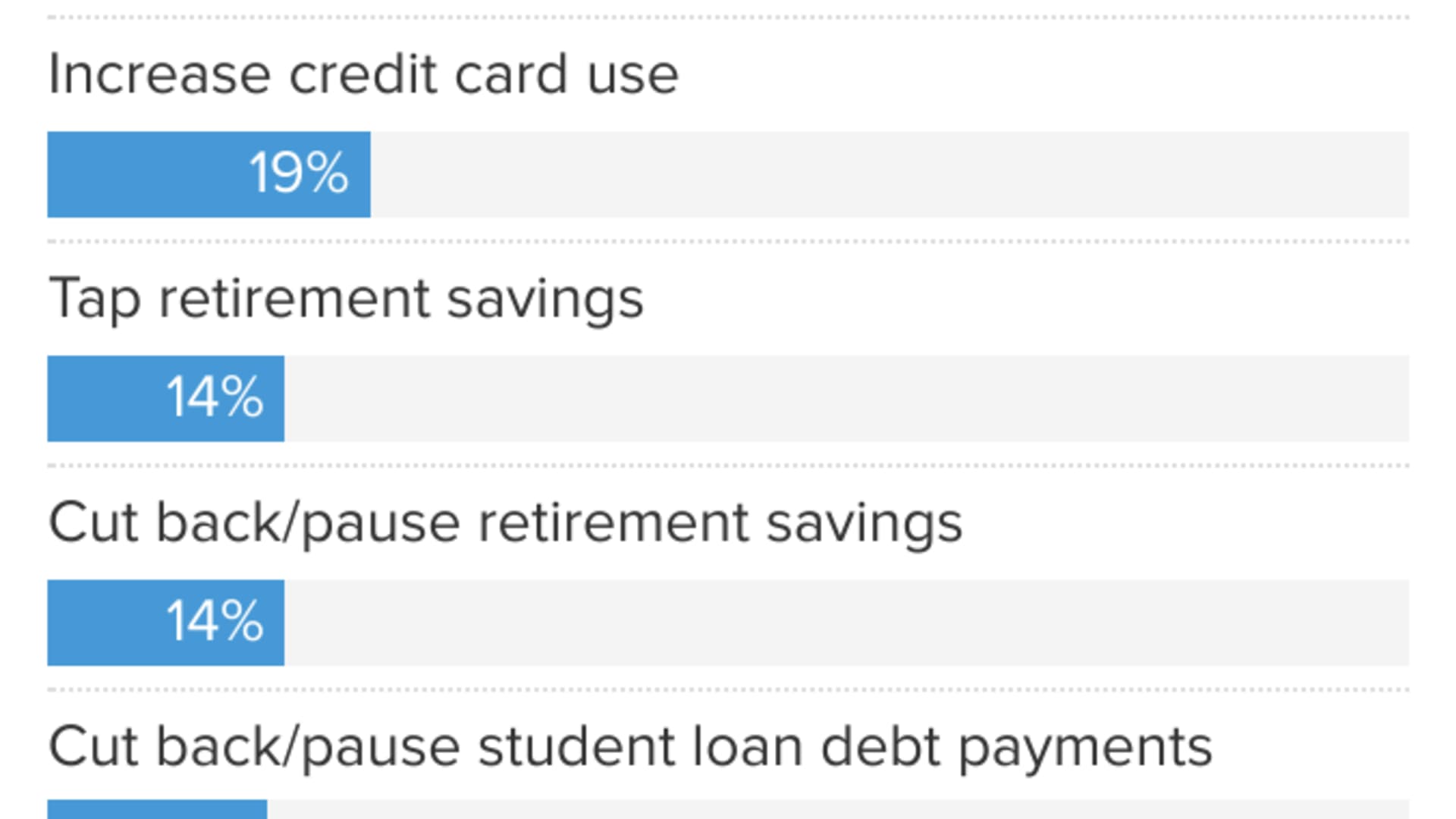

To bridge the gap, Americans are dipping into their savings accounts and running up credit card balances. That leaves them more financially vulnerable in the event of an economic shock.

With economists now forecasting a possible recession, 62% of middle-income households said they need to get financially prepared, Primerica also found.

“Unfortunately, I think it is only going to get worse,” Ted Jenkin, CEO at Atlanta-based Oxygen Financial and a member of CNBC’s Advisor Council, said of Americans' financial standing.

Hope for the American dream is at an all-time low, especially among the middle class, according to the latest Gallup poll, which tracks Americans' assessments of the next generation's likelihood of surpassing their parents' living standards.

Now, 59% of middle-income Americans — or those making between $40,000 and $100,000, according to Gallup — said it is very or somewhat unlikely that today’s young adults will have a better life than their parents compared to only 48% of those with annual household incomes under $40,000 who feel that way.

Amid inflation, 'you really have to get disciplined'

"As middle-income families prepare for a possible recession this year, it's more vital than ever that they take control of their personal finances by addressing debt, setting a budget and keeping spending in check," Glenn Williams, Primerica's CEO, said in a statement.

Experts often recommend starting with high-interest credit card debt. Credit card rates, in particular, are now more than 19%, on average — an all-time record. Those annual percentage rates will keep climbing, too, as the Federal Reserve continues raising its benchmark rate.

If you currently have credit card debt, tap a lower-interest personal loan or 0% balance transfer card and refrain from putting additional purchases on credit unless you can pay the balance in full at the end of the month and even set some money aside.

“You really have to get disciplined or you’re going to outspend your income,” Jenkin said.

To curtail your spending, Jenkin said some simple financial hacks can help, such as going to the grocery store less and cutting back on online shopping.

“Grocery stores are just like Las Vegas; they are there to separate you from your wallet.” Meal planning is one way to edit down your shopping list to weekly essentials and save money.

Disabling one-click ordering or deleting stored credit card information can also help. “Anyone that shops on Amazon and has a stored credit card, you are basically pouring lighter fluid on your budget,” Jenkin said.

Jenkin recommends waiting 24 hours before making an online purchase and then using a price-tracking browser extension such as CamelCamelCamel or Keepa to find the best price.

Finally, tap a savings tool like Cently, which automatically applies a coupon code to your online order, and pay with a cash-back card such as the Citi Double Cash Card, which will earn you 2%.