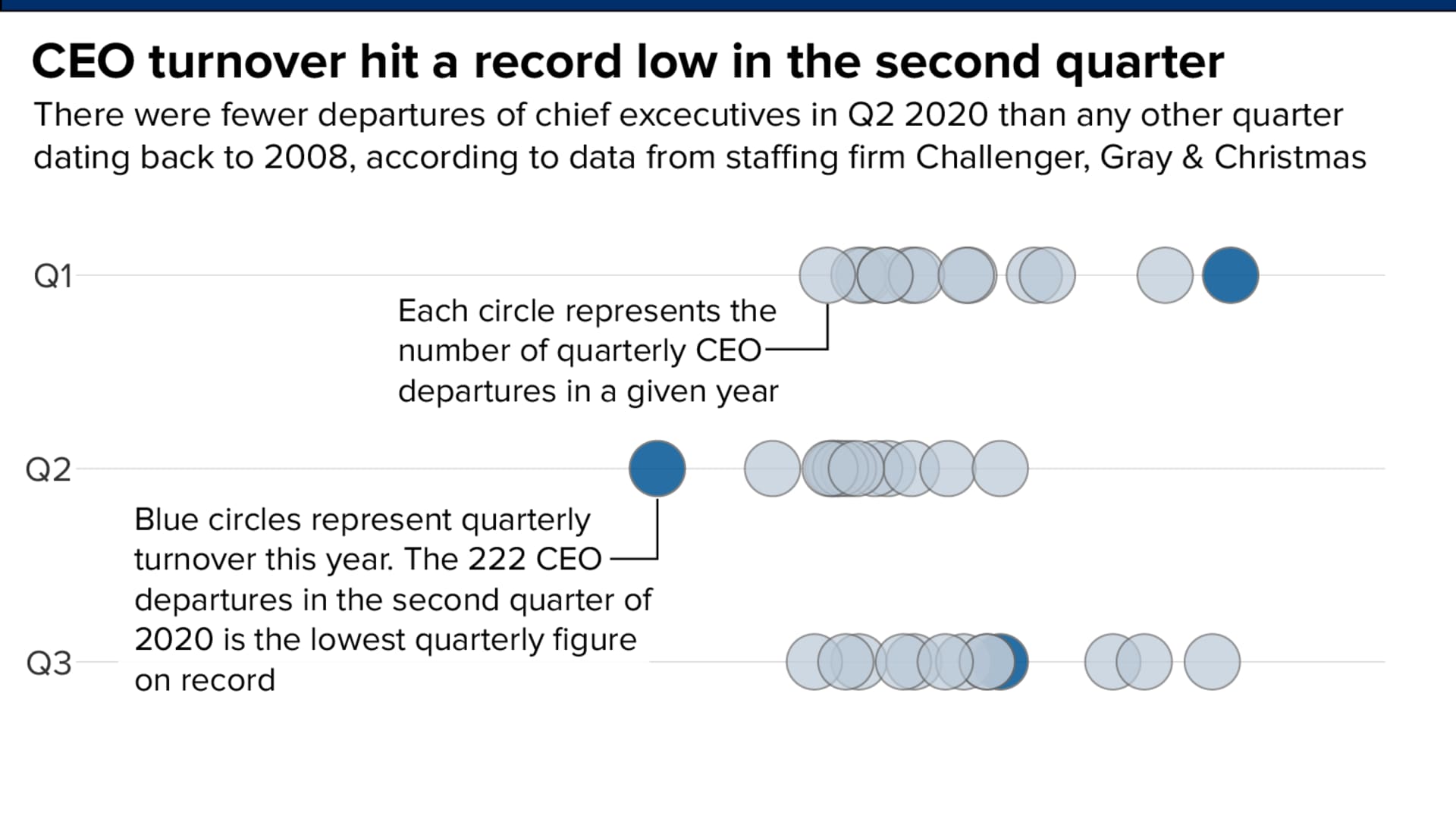

- Only 71 companies in the Russell 3000 Index changed CEOs in the second quarter, 11% lower than the average turnover in the two prior years, a new study from the Conference Board provided exclusively to CNBC shows.

- The Covid-19 crisis created a host of new problems for corporate boards to deal with, and they likely wanted to avoid any additional uncertainty.

- The remote work environment has also made it a particularly bad time to conduct a search for a new executive, which typically involves lots of in-person meetings.

As the coronavirus pandemic ravaged the economy in the second quarter of this year, corporate boards opted for stability in leadership, driving CEO turnover to its lowest level in years.

A new study from The Conference Board provided exclusively to CNBC shows that only 71 companies within the Russell 3000 Index announced CEO changes in that period, 11% lower than average turnover in the two prior years. Additional data from staffing firm Challenger, Gray & Christmas shows that the second quarter was the lowest quarter for CEO turnover since 2008, as far back as its data goes.

"It's like people eating comfort food," said Rosabeth Moss Kanter, a Harvard Business School professor. With the onset of the pandemic and corresponding economic crisis making so much unknown, employees "need to hear from someone they know and respect about what's going on" and companies want to "minimize additional sources of uncertainty."

A change in leadership is one of the most significant events that can take place at a company, with effects on its operations, culture and reputation, said Matteo Tonello, managing director of ESG Research at The Conference Board.

"In a situation that is as extraordinary as the Covid crisis, companies found themselves having to make a decision on whether they want to compound business risks with additional uncertainty," said Tonello, who authored the study alongside ESG data analytics firm Esgauge and executive search firm Heidrick & Struggles.

Money Report

He noted that a Conference Board survey in April found a majority of senior executives said their crisis preparedness plans were inadequate to address the situation caused by the pandemic, indicating that corporate boards faced a long list of business challenges they had to react to and balance with any CEO succession plans.

"If you're a board member, your agenda is pretty full: cash flow, figuring out work from home," said David Larcker, director of the Corporate Governance Research Initiative at the Stanford Graduate School of Business. "The last thing you need is having a bunch of people at the top leave."

A postponed retirement

Greenbrier, an Oregon-based supplier of railroad freight car equipment, explicitly referenced the pandemic as the reason CEO Bill Furman postponed his retirement to stay on with the company for two more years.

"The current COVID-19 crisis and accompanying environment of economic uncertainty requires an experienced industry and management team to lead Greenbrier through extraordinary times," the company said in a July 10 press release that announced Furman's September 2022 retirement date. "Effective management through the pandemic and the current economic uncertainty is the company's most pressing priority."

In April, Greenbrier responded to the slowing economy by suspending rail car production and laying off about 200 employees at its Greenbrier Gunderson manufacturing facility. By the time its fiscal 2020 ended on Aug. 31, the company shuttered 13 rail production lines and reduced its global workforce by more than 6,500 employees, or by about 40%, including both staff and production employees. The company said it had to be nimble to control its costs.

Even if a company wanted to replace its CEO, the search would have been much more difficult in the second quarter. The process, especially for companies entertaining outside candidates, would have been challenged by the abrupt switch to a remote working environment.

Jeff Sanders, who co-leads the CEO and corporate board search practice at Heidrick & Struggles, said that much of the pre-pandemic executive search process relied on face-to-face interaction. The question boards face now, he said, is how to make a hiring decision without meeting in person. While it's easy to make initial contact with candidates over video, the later stages of the search process are slower as they seek ways to make up for a lack of time spent together during the hiring process.

Despite the second-quarter decline in turnover, 71 Russell 3000 companies did carry out successions in that period, which overlapped with the first peak of Covid-19. Larcker said that individual circumstances for some companies may have been bad enough to justify a change.

"When things are in disarray, maybe the board has been thinking about this for a while, doesn't like some choices that are made and says 'look, there is a lot going on, we're going to push someone out,'" he said. "Most people, I think, come back and say 'we don't need another major thing to deal with' unless it's really bad."

CEO turnover picks up

While The Conference Board study does not cover events after the second quarter, the Challenger, Gray & Christmas data is current as of October and shows a rebound in successions to levels in line with prior years.

Heidrick & Struggles has seen a pickup in searches since the summer, Sanders said, suggesting that companies and their boards have adapted to, or at least accepted the reality of, the way business is conducted amid a pandemic.

"By the summer, while the pandemic still raged, there was a veering back toward conditions that were a little more certain," said Harvard's Kanter. She said that by that time there was a better understanding of the safety precautions that needed to be taken to curb the virus's spread and that brought the business world a little closer to what was once considered normal. At the minimum, she said, "it was possible to make business decisions again."

BlackLine, a Los Angeles-based provider of accounting software, announced plans in August to promote its president, Marc Huffman, to CEO. He will take the reins from founder Therese Tucker at the beginning of next year.

The company said the Covid crisis didn't change its timing. A multiyear succession plan was in place to allow Huffman to gradually accrue responsibility and take on a more visible role alongside Tucker. Recently, he has taken over the majority of direct employee communication duties, for example.

"We chose to look at it as an opportunity," Huffman said about the health crisis. "There was so much that got tossed up in the air. Everybody is looking for leadership and a voice."

But, Huffman and Tucker both said it would be unthinkable for an external hire to take over as CEO in the current environment. Huffman had the advantage of already being with the company for two years, building up an understanding of its culture and strategy.

"You throw the pandemic into it and it's probably impossible," said Huffman. "I can't imagine trying to take over a company externally via Zoom."