Almost everyone wants to get better with money, whether that means earning more, spending less, or building generational wealth. And with April marking the beginning of Financial Literacy Month, it's a great time to take stock of your personal finances and develop a plan to improve them.

To help get you started, CNBC Make It compiled a 30-day money challenge, with simple, actionable tips you can follow every day of the month to boost your savings, tackle your debt, and get smarter with your money.

Day 1: Identify your money goals and values

The first step to managing your money well is knowing how you want it to work for you. Take some time to think through what's most important to you, then distill those values into clear goals.

Get Boston local news, weather forecasts, lifestyle and entertainment stories to your inbox. Sign up for NBC Boston’s newsletters.

Remember, this should reflect what actually matters to you, not what you think should matter.

"You need to attach a 'why' and your values behind your financial goals as opposed to just 'I was told I should buy a house by my parents, maybe I should do that,'" Tori Dunlap, founder of Her First $100K, previously told CNBC Make It. "If you don't want to do that, don't do it. That's OK. You need to find things that actually reflect your values."

Money Report

Day 2: Find an accountability buddy

Your financial goals don't mean much if you don't stick to them. Share them with a friend or family member who can hold you accountable to following through, whether your goal is as big as getting together a down payment or as small as knocking a bit off your grocery bill.

"We can actually guilt ourselves into being a little smarter with our finances when we're doing it with a buddy," Vivan Tu, founder of "Your Rich BFF," previously told CNBC Make It.

Day 3: Open a high-yield savings account

If your savings are sitting in a traditional savings account, you probably aren't earning much interest. You could bring in around 1,600% more in interest by switching to a high-yield account, which currently boast rates around 4%, compared with just 0.23% for traditional accounts. That's the difference between earning $400 in interest per year versus $23.

Day 4: Start saving for a short-term goal

Now that you have a a list of goals and an interest-bearing savings account, start putting away funds for a short-term goal, such as a vacation or wedding. It's OK to start small; getting into the habit of regularly saving takes time.

Day 5: Figure out how long it will take you to get out of debt

The first step toward eliminating debt is knowing where you stand. Once you have an idea of how much you need to pay each month to be debt-free, you can create a plan.

CNBC Make It's loan calculator can help you estimate your monthly payment, how long it will take to pay off the debt and how much you'll pay in interest.

Day 6: Start building an emergency fund

Setting aside money in a so-called emergency fund will help you cover unexpected expenses, such as a car repair or surprise medical bill, without taking on debt. Most experts recommend socking away enough to cover three to six months worth of living expenses, but starting with whatever you can will help provide a financial cushion.

Day 7: Calculate your credit utilization ratio

You may be unfamiliar with your credit utilization ratio, but it accounts for up to 30% of your credit score. This ratio represents how much of your available credit you're using at any given time. The lower you can keep it, the better, because it shows lenders that you're able to pay back what you owe in a timely manner.

To determine your own credit utilization ratio, add up the credit limits for all of your credit cards, then divide your monthly spending by that figure. If it's higher than 30%, you may want to find ways to bring it down.

Day 8: Audit your subscriptions

One of the easiest ways to lower your monthly expenses is to cut out any subscriptions you're paying for but not actually using. Take a look at your credit card statements for the past 12 months. Are there any recurring payments you no longer need? If so, take a few minutes to cancel.

Don't forget to look out for subscriptions that renew annually, rather than monthly, as well.

Day 9: Automate your savings

Make saving money seamless by setting up automatic contributions to your emergency fund or other savings account through your employer's direct deposit system.

″'Out of sight, out of mind' applies here," Katherine Fox, a certified financial planner based in Portland, Oregon, previously told CNBC Make It. "If you don't see the money deposited into your regular checking account, you are less inclined to think of it as money that is 'yours' to spend."

Day 10: Evaluate your car insurance coverage

With inflation persistently high, your car insurance coverage may not go as far as it used to. Review your policy to make sure you're adequately covered, especially in terms of liability coverage, which covers damage to property or other vehicles, as well as medical expenses for other drivers and any lawsuits you may face.

And it doesn't hurt to shop around and make sure you're getting the best price.

Day 11: Check your credit score

The higher your credit score, the better the interest rates you'll qualify for on new credit cards and loans, including a mortgage or auto loan. That's because your credit score tells lenders how trustworthy you are when it comes to paying back borrowed funds.

There are a number of ways to check your score for $0, starting with your credit card issuer or bank, many of which offer free services to their clients.

Day 12: Make the most of your subscriptions

If you're paying for subscriptions like Amazon Prime, you may be entitled to more perks than you're actually using. Take a few minutes to read the fine print on your memberships, so you don't miss out on extra benefits you're not aware of.

Day 13: Fund your health savings account

If you're enrolled in a health savings account, or HSA, don't forget to fund it. For 2023, you can contribute up to $3,850 for a single individual and up to $7,750 for a family.

Not only does money put in an HSA lower your taxable income, but your contribution then grows tax-free, and as long as you spend it on qualified medical expenses, you won't pay tax when you withdraw, either.

Day 14: Sign up for a personal finance newsletter

One of the easiest, and cheapest, ways to learn about money is to get a personal finance newsletter (or two, or three) delivered straight to your inbox. They often include clear and actionable advice, and will keep your finances top of mind.

Make It's own money newsletter goes out every Wednesday.

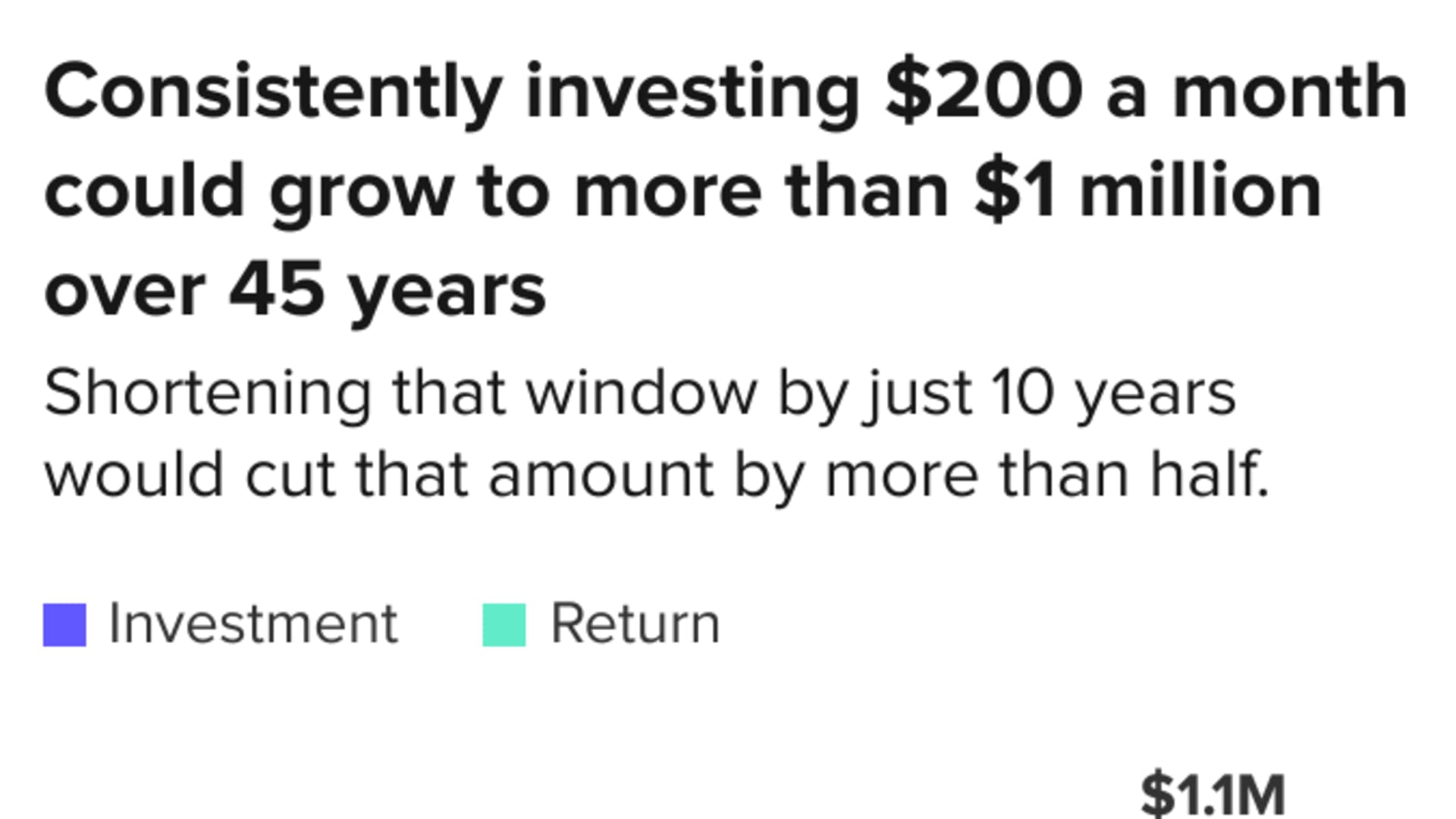

Day 15: Start investing

If you aren't already investing in the stock market, whether through an employer-sponsored retirement account or taxable brokerage account, there's no time like the present to start. That's because "the greatest money-making asset anyone can possess is time," Ed Slott, publisher of IRAHelp.com, previously told CNBC Make It.

The earlier you start investing, the more time your money has to grow and compound.

Day 16: Update your income with your credit card company

If you've received a raise or promotion since opening your credit card, consider reporting your increased income to your lender. You'll likely qualify for an automatic credit limit increase on your existing loans or credit cards, which could, in turn, raise your credit score. If the limit increase isn't automatic, you can request one with your bank or lender.

It doesn't hurt to try asking for a lower interest rate, either.

Day 17: Try reverse budgeting

If traditional budgeting methods haven't worked for you, give "reverse budgeting" a try. It's simple: Start by putting 20% of your income toward financial goals, such as paying down debt or saving for retirement. Next, cover all of your fixed, necessary expenses, such as rent and your phone bill.

That's it — the rest of your money is available to spend guilt-free.

Day 18: Put your tax refund to good use

If you received a tax refund this year, you may be tempted to spend it on a vacation or a new video game. But that windfall can help you jumpstart a number of financial goals, such as building an emergency fund, saving for retirement or putting money away for your a child's college education.

Challenge yourself to put at least part of it toward something practical.

Day 19: Take a step toward eliminating your debt

If you're struggling to pay off your credit card debt, you may be able to get rid of it faster by consolidating the debt using a personal loan. You use the loan to pay off your credit card balances, then concentrate on paying down the loan itself, which typically has a much lower interest rate.

Another option is a balance transfer card, which allows you to move your debt from a credit card with a high annual percentage rate (APR) to one with a 0% APR introductory period that typically lasts up to 21 months.

Day 20: Re-evaluate your prescriptions

You may be overpaying for your prescriptions, especially if you order through a trendy online marketplace. Take a few minutes to compare prices online and see if you're getting a good deal. Free coupons at sites such as GoodRx and ScriptSave WellRx can help cut down costs.

It's worth seeing how much the same prescription would cost through your doctor, or if they're able to recommend a cheaper alternative.

Day 21: Diversify your income streams

It's never been easier to boost your income through part-time work. A number of side hustles draw on skills you already have, can be done remotely, and pay as much as $100 per hour.

You may be able to earn passive income by renting out property you already own or monetizing your social media.

Day 22: Tackle a financial task you've been avoiding

We all have that one lingering financial task on our to-do list that we keep putting off. Let get it done. Whether it's rolling over your 401(k) from a previous job or updating your budget, you'll feel better knowing it's out of the way.

Day 23: Review your rewards credit cards

Rewards credit cards offer valuable benefits, such as cash back and discounts on travel, but often come with annual fees that can cost hundreds of dollars. Ask yourself three simple questions to determine if you're getting your money's worth or if it's time to cancel or downgrade your card.

- Are you using your rewards card correctly?

- Do your card's rewards match your spending habits?

- Does the card's statement credits or welcome bonus offset the annual fee?

Day 24: Re-assess the funds you own

Mutual funds can be a low-cost way to diversify your investments — but they're not all created equal. Go through your portfolio and take note of any funds with high fees or lagging performance. Those may require a closer look to determine if they're worth holding onto.

You may want to work with a financial professional, who can help parse any tricky financial jargon and assist with finding more suitable investments.

Day 25: Calculate your savings rate

If you have a big money goal in mind, such as buying a home or retiring early, you should have a solid understanding of where your money is going, including how much you're actually saving.

An easy way to do that: Calculate your savings rate, which is the percentage of your income that you keep each month, versus the amount that you spend.

Day 26: Score discounts on things you're already buying

Even if you don't own a car, it may be worth signing up for a AAA membership to take advantage of discounts on hotels, rental cars, electronics and prescription lenses.

Similarly, AARP offers members discounts on dining out, entertainment, travel and more — and anyone of any age can join.

Day 27: Increase your 401(k) contribution

Experts typically recommend setting aside 10% to 15% of your income for retirement. If that seems easier said than done, start with what you can afford and gradually increase your contribution by 1% at a time, starting today. Even a small boost can add up over time.

Plus, most providers allow you to set your contributions to auto-increase, so they'll automatically go up each year — and you probably won't even miss the money.

Day 28: Look into dividend stocks

If you already invest regularly and want to take the next step to boost your portfolio, consider adding dividend-paying stocks, which offer regular cash payouts that you can either reinvest or use as income. But be sure to check in with your financial planner or other professional before making any major changes to your portfolio.

Day 29: Create a 'conscious spending plan'

It's important to know where your money is going, but it can be tedious to track every penny. Instead, create a "conscious spending plan," which focuses on four numbers, as recommended by Ramit Sethi, author of the New York Times bestseller "I Will Teach You To Be Rich."

- Fixed costs, such as your rent or student loan payments

- Savings, including your emergency fund and money for vacations

- Investments, such as your 401(k) or Roth IRA contributions

- "Guilt-free spending," such as ordering food or shopping

Day 30: Pick up a personal finance book

Keep your financial education going past the 30-day mark with a book on investing, building wealth or whichever topic you want to learn more about.

Steve Adcock, a self-made millionaire who retired at 35, recommends classics like "Your Money or Your Life" by Vicki Robin and Joe Dominguez and "The Millionaire Next Door" by Dr. Thomas Stanley, among others.

Additional reporting by Alicia Adamczyk, Cheyenne DeVon, Ryan Ermey, Gili Malinsky, Kamaron McNair, Morgan Smith, Nicolas Vega and Mike Winters.

DON'T MISS: Want to be smarter and more successful with your money, work & life? Sign up for our new newsletter!

Take this survey and tell us how you want to take your money and career to the next level.