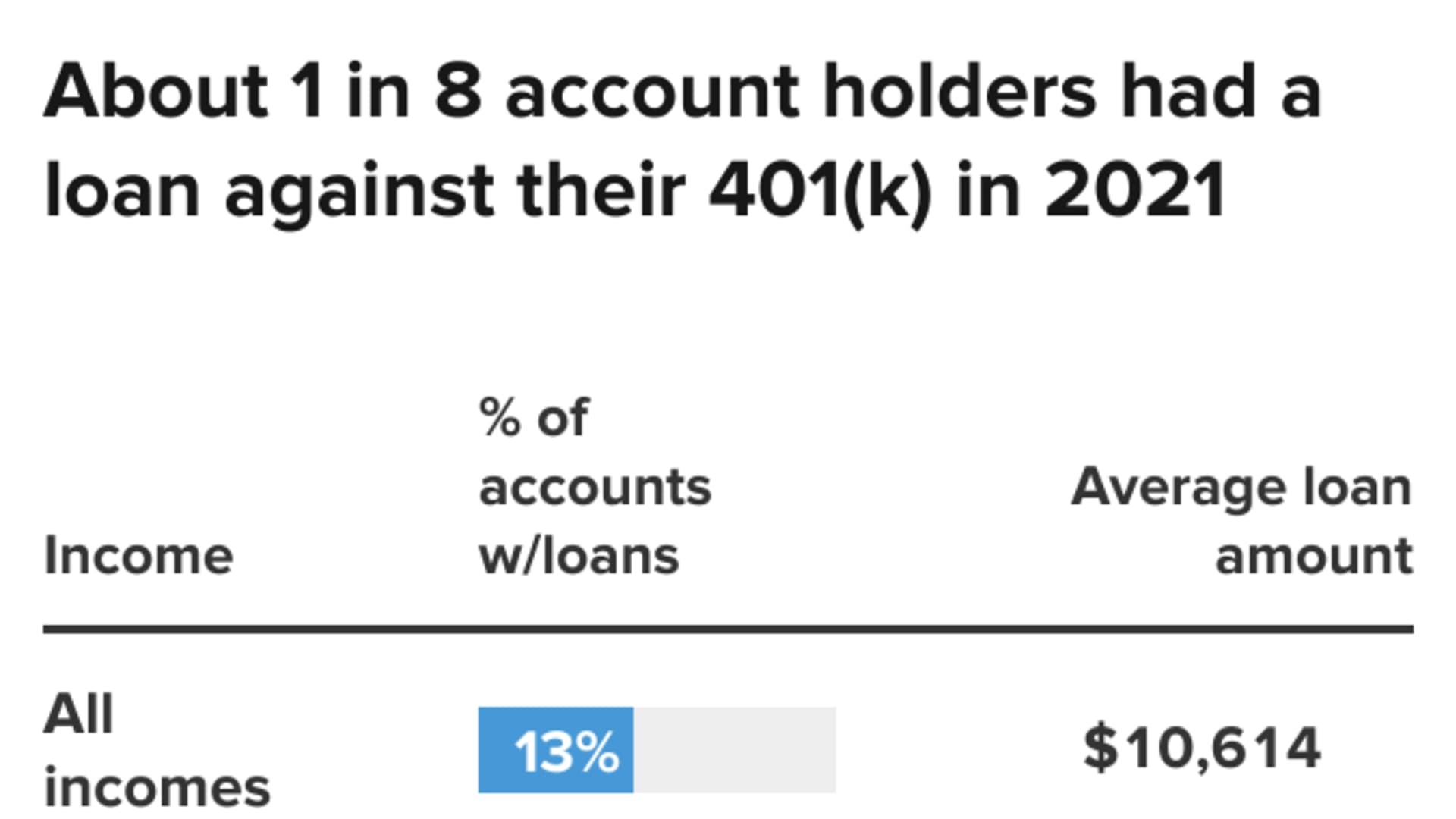

- Roughly 13% of 401(k) participants had a loan outstanding last year, with an average balance of $10,614, according to new research.

- Depending on the specifics of your company's plan, you might be required to pay off the loan right away when you leave your job.

- Here's how to avoid a tax bill if your company ends up considering the loan balance a distribution.

If you're heading to a new job and still owe money on a 401(k) plan loan from your former employer's retirement savings plan, be sure you know what will happen to that outstanding balance.

While you may be permitted to continue paying off the loan in installments, most companies expect immediate repayment when you leave. And if you don't fork over what's owed, it can result in an unexpected tax bill.

"Typically, if you have a loan and leave your job, you're supposed to pay back the loan within a short time period," said certified financial planner Avani Ramnani, managing director for Francis Financial in New York. "If you don't, it's considered a distribution with tax [consequences]."

Get Boston local news, weather forecasts, lifestyle and entertainment stories to your inbox. Sign up for NBC Boston’s newsletters.

Last year, roughly 13% of 401(k) participants had a loan outstanding, according to Vanguard's How America Saves 2022 report, which was released Tuesday. While largely unchanged from 2020, the share is down from 16% in 2016.

The average balance on those loans is $10,614 and is most common among workers with incomes from $30,000 to $100,000. About 81% of plans allow loans, whose repayment terms typically are five years.

Money Report

Also, 401(k) loan use is highest among participants age 45 to 54, at 18%, Vanguard's report shows. That's followed by 15% in the 35-to-44 age cohort and 13% for those 55 to 64.

Federal law allows workers to borrow up to 50% of their account balance, with a maximum of $50,000. (In 2020, that cap was temporarily increased to $100,000 for loans initiated due to Covid-related reasons.) The loan is tax-free and, unlike with most outright distributions, there is no early withdrawal penalty of 10% if you're under age 59½.

However, when you leave your job — whether by choice or not — the tax treatment can change.

As mentioned, if your plan requires you to repay the money right away and you don't, your account balance will be reduced by the amount owed. This so-called "loan offset" is considered a distribution subject to ordinary income taxes and potentially the 10% early-withdrawal penalty.

More from Personal Finance:

Emergency savings take a hit as households adjust finances

Key things financial advisors would tell their younger selves

Health insurers poised to pay $1 billion in rebates this year

Yet if you can come up with what you owe, you can essentially roll over the loan offset amount to an individual retirement account or another eligible plan and avoid the tax consequences.

You get until the federal tax deadline the following year to do so — i.e., if you leave your job in June 2022, you generally would get until April 18, 2023, to come up with the funds for the rollover (although if you file a tax extension, you'd get longer).

Prior to major tax law changes that took effect in 2018, participants only had 60 days.