- President-elect Biden will give student loan borrowers more time before they have to resume payments, an aide said last week.

- Yet one key detail was missing from the announcement: How much more time?

- "Federal student loan borrowers are in limbo right now," said Anna Helhoski, a student loan expert at NerdWallet.com.

An aide for the incoming Biden administration said last week the president-elect will extend the payment pause and interest waiver for student loan borrowers beyond this month, when it was set to expire.

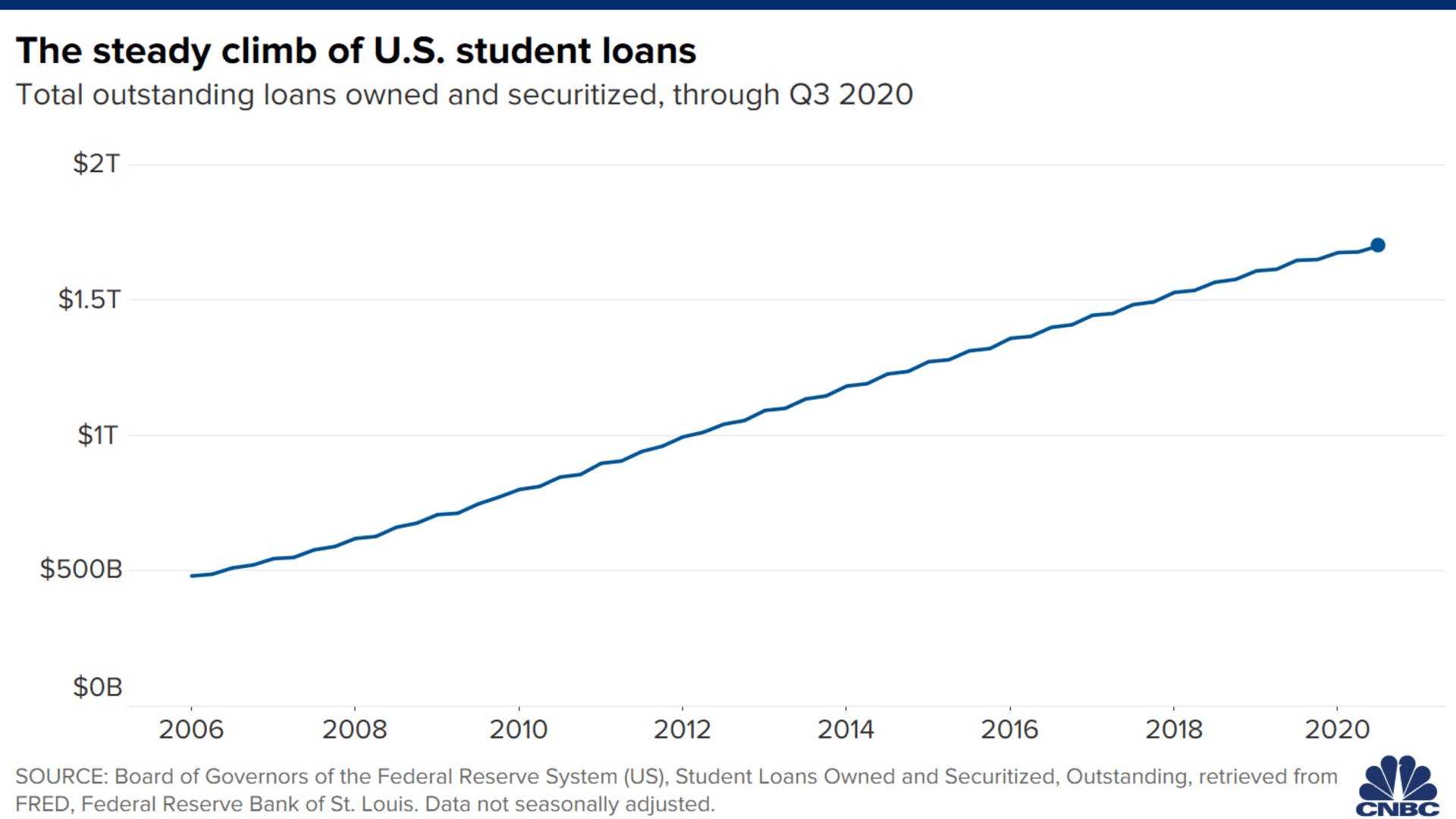

That means the 42 million Americans with federal student loans will have more time before they need to start making their monthly payments again.

Yet one detail was missing from the announcement: How much more time?

"Federal student loan borrowers are in limbo right now when it comes to payment restarting again," said Anna Helhoski, a student loan expert at NerdWallet.com.

Despite the current uncertainty, here are some answers to questions you might have.

Money Report

How long will the extension be?

Without the Biden administration detailing how long an extension, all experts can do is speculate.

"I'm hearing everything from April to September," said Betsy Mayotte, president of The Institute of Student Loan Advisors, a nonprofit that helps student loan borrowers with free advice and dispute resolution.

Higher education expert Mark Kantrowitz said he believes the pause will last until the end of September 2021.

"Other proposals are not nearly long enough, given that the pandemic and its economic aftershocks will not be over by then," he said.

How can I prepare to begin repayment?

A lot has changed this year.

Make sure your lender has your most recent contact information, including email and address, said Scott Buchanan, executive director of the Student Loan Servicing Alliance, a trade group for the companies.

"You can confirm we have the right info by just logging in to your account online," he said. "That way, you will hear directly from your servicer with all the relevant information on when you will resume repayment."

What if I'm pursuing Public Service Loan Forgiveness?

Public service loan forgiveness was signed into law by President George W. Bush in 2007 and allows certain not-for-profit and government employees to have their federal student loans forgiven after 10 years.

Each month during the payment pause still counts toward the 120 payments you need to make to get your student loans canceled through the program. That means it doesn't make sense for you to continue paying down your loans during the reprieve, even if you can afford to.

I'm worried I won't be able to pay my bill

Borrowers who've lost their jobs or had their pay cut because of the Covid pandemic have options when bills come due again.

You can enroll in an income-driven repayment plan, which caps your monthly payment at a portion of your earnings and some bills wind up being as little as $0. As with public service, the months during the payment pause also count toward your eventual debt forgiveness.

Borrowers may also want to ask their servicers about an economic hardship or unemployment deferment.

More from Personal Finance:

Covid is making it harder to get into a top college

Here's how delaying college may impact your future earnings

College can cost as much as $70,000 a year

What if I have private student loans?

The government's payment pause only applies to federal student loans. For the millions of Americans with private student loans, the bills are still due.

Some private lenders offered borrowers relief options early in the pandemic. Unfortunately, many of those programs have dried up, Mayotte said.

Still, it can't hurt to ask your lender for help.

"If a borrower is struggling with their private loans, their best advice is to contact their private loan servicer directly as most don't advertise the options for relief they do offer," she said.

I'm still working. What should I do with the extra money?

If you haven't faced major financial setbacks during the pandemic, it might make sense to continue making payments on your student loans while interest is suspended.

"These payments will go entirely to principal, helping them pay down their debt quicker," Kantrowitz said.

But first you should consider creating an emergency savings fund with half a year's salary, he added: "They may have their job now, but who knows what might happen in a month or two?"

If you already have a healthy savings account, use the extra cash to pay down any private loans or credit card debt, experts say.